As Bitcoin and other cryptocurrencies have grown in popularity, attention has shifted to blockchain, the underlying distributed ledger technology (DLT) that drives them.

At its core, blockchain technology is easy to comprehend. Essentially, the technology consists of a shared database with entries verified and encrypted via peer-to-peer networks. To kickstart your crypto venture, you’d need help with the capital and this is where playing UFABETสมัคร online would come in handy.

It’s helpful to envision it as a strongly encrypted and verified shared Google Document. Each entry in the sheet depends on a logical relationship to all its predecessors and is agreed upon by everyone in the network.

However, blockchain technology has many more applications than merely serving as the fuel for Bitcoin. In this article, we’ve listed some of the technology’s emerging uses in banking, business, government, and other fields. But first, let’s talk about how a blockchain actually works.

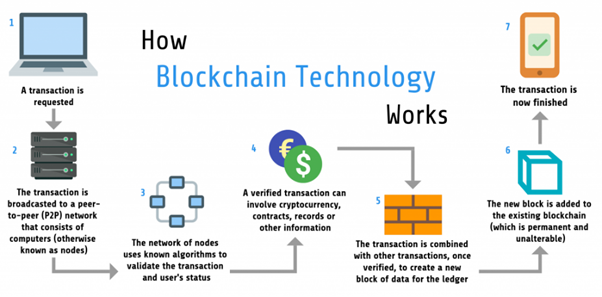

How Blockchains Work

Blockchains are also known as distributed Ledger Technology (DLT). The objective of blockchain technology is to enable the recording and distribution of digital data without the ability to modify it. In this sense, a blockchain serves as the foundation for immutable ledgers or transaction records that can’t be changed, erased, or destroyed.

Every transaction is a digital ‘block’ that must be confirmed before it can be accepted into the system through mining. This process involves the use of computing systems that compete to solve mathematical puzzles using specialized processors. The first miner to solve the challenge is awarded Bitcoin. In addition, the mining process verifies and trusts transactions on the cryptocurrency’s network.

For protocols that operate on the PoS consensus, blocks are produced through staking of token holdings rather than computational power. For instance, Moonbeam parachain validates transactions and secure its network using the Nominated Proof OF Stake model (NPoS). This model depends on three major players: the collators, validators and delegators.

- Validators: They secure the Relay Chain by staking Polkadot.

- Collators: The best moonbeam collators are selected to be block producers. They maintain the parachain (Moonbeam) by collecting transactions from users to produce state transition proofs for the relay chain to validate.

- Delegators: Cryptocurrency holders stake their tokens, vouching for specific collator candidates. Any user that holds a minimum number of tokens is eligible to become a delegator.

These mechanisms reduce fraud by eliminating the possibility of double-spending or spam, and they also make money transfers simple, secure, and fast.

Real-World Blockchain Use Cases

Application in healthcare

The collation of data generated by linked medical equipment is a major concern right now, but blockchain could be the bridge that connects those silos. Blockchain can connect specialized medical equipment with a person’s health record as they become more common and increasingly linked to that record. Devices will save and attach data collected on a healthcare blockchain to personal medical records.

General information like age and gender and basic medical history data like immunization history or vital signs are examples of health data that is ideal for blockchain. None of this data can be used to identify a specific patient on its own, which is why it can be maintained on a shared blockchain that a large number of people can view without causing privacy concerns.

Blockchain use cases for Governments

While simultaneously improving trust and accountability, a blockchain-based digital government can protect data, improve operations, and eliminate fraud, waste, and abuse. Individuals, organizations, and governments share resources on a distributed ledger secured by cryptography in a blockchain-based government model. This design avoids a single point of failure and safeguards critical public and government data from the start.

A blockchain-based government can address long-standing issues and provide the following benefits:

- Record Management: Individual data, such as birth and death dates, marital status, and property transactions, are maintained by the federal, state, and local governments. However, organizing this data can be problematic, and some of these documents are still only available on paper. Residents may be required to physically visit their local government offices in order to make changes, which is often time-consuming, inefficient, and inconvenient. Blockchain technology has the potential to make recordkeeping easier and data more secure.

- Voting: Blockchain technology has the potential to make voting more accessible while also increasing security. Hackers would have no chance against blockchain technology since they wouldn’t affect other nodes even if they gained access to the terminal. Each vote would be associated with a single ID, and because creating a false ID would be difficult, government employees would be able to tally ballots more swiftly and effectively.

- Taxes: With enough data recorded on the blockchain, the time-consuming process of filing taxes, which is prone to human mistakes, might become considerably more efficient.

Supply Chain and Logistics Tracking

There are various advantages to using blockchain technology to track products as they transit through a logistics or supply chain network. First and foremost, because data is stored on a secure public ledger, it facilitates communication between partners. Second, because the data on the blockchain cannot be changed, it provides higher security and data integrity. As a result, logistics and supply chain partners may collaborate more freely.

Blockchain Use Cases in Banking & Finance

International Remittance

Blockchain enables the creation of a tamper-proof log of sensitive activity securely and efficiently. This attribute makes It ideal for international payments.

PayPal and other peer-to-peer payment platforms are handy, but their services are often limited to geographical locations. Others levy exorbitant fees for their services., while many are also vulnerable to hackers, which is unappealing to clients required to provide personal financial information. Blockchain technology has the potential to remedy these hurdles, and crypto-based remittance companies like Telcoin and Banco Santander are maximizing this potential.

Banco Santander introduced the first blockchain-based money transfer service in April 2018. The service, dubbed “Santander One Pay FX,” makes international money transfers same-day or next-day using Ripple’s xCurrent. Santander has decreased the number of intermediaries traditionally necessary in these transactions by automating the entire process on the blockchain, making the process more efficient.

Insurance

Smart contracts are arguably the most important blockchain application for insurance. Customers and insurers can manage claims clearly and securely thanks to these contracts. All contracts and claims may be stored on the blockchain and authenticated by the network, which would reduce invalid claims by rejecting numerous claims for the same accident.

For example, openIDL, a network created in collaboration with the American Association of Insurance Services and implemented on the IBM Blockchain Platform, automates insurance regulatory reporting and streamlines compliance procedures.

Concluding Thoughts

Although blockchain technology has been adopted across many sectors, industry experts believe we are still in the early stages of mass adoption of this cutting-edge technology.

Comments